Classical Economist

The classical economists believed in the existence of full employment in the economy. To them, full employment was a normal situation and any deviation from this regarded as something abnormal. According to Pigou, the tendency of the economic system is to automatically provide full employment in the labour market when the demand and supply of labour are equal.

Unemployment results from the rigidity in the wage structure and interference in the working of free market system in the form of trade union legislation, minimum wage legislation etc. Full employment exists “when everybody who at the running rate of wages wishes to be employed.”

Those who are not prepared to work at the existing wage rate are not unemployed because they are voluntarily unemployed. Thus full employment is a situation where there is no possibility of involuntary unemployment in the sense that people are prepared to work at the current wage rate but they do not find work.

The basis of the classical theory is Say’s Law of Markets which was carried forward by classical economists like Marshall and Pigou. They explained the determination of output and employment divided into individual markets for labour, goods and money. Each market involves a built-in equilibrium mechanism to ensure full employment in the economy.

Assumptions:

classical theory of output and employment is based on the following assumptions:

1. There is the existence of full employment without inflation.

2. There is a laissez-faire capitalist economy without government interference

3. It is a closed economy without foreign trade.

4. There is perfect competition in labour and product markets.

5. Labour is homogeneous.

6. Total output of the economy is divided between consumption and investment expenditures.

7. The quantity of money is given and money is only the medium of exchange.

8. Wages and prices are perfectly flexible.

9. There is perfect information on the part of all market participants.

10. Money wages and real wages are directly related and proportional.

11. Savings are automatically invested and equality between the two is brought about by the rate of interest

12. Capital stock and technical knowledge are given.

13. The law of diminishing returns operates in production.

14. It assumes long run.

Says law

Say’s law of markets is the core of the classical theory of employment. An early 19th century French Economist, J.B. Say, enunciated the proposition that “supply creates its own demand.” Therefore, there cannot be general overproduction and the problem of unemployment in the economy.

If there is general overproduction in the economy, then some labourers may be asked to leave their jobs. The problem of unemployment arises in the economy in the short run. In the long run, the economy will automatically tend toward full employment when the demand and supply of goods become equal.

When a producer produces goods and pays wages to workers, the workers, in turn, buy those goods in the market. Thus the very act of supplying (producing) goods implies a demand for them. It is in this way that supply creates its own demand.

Determination of Output and Employment:

In the classical theory, output and employment are determined by the production function and the demand for labour and the supply of labour in the economy. Given the capital stock, technical knowledge and other factors, a precise relation exists between total output and amount of employment, i.e., number of workers. This is shown in the form of the following production function: Q=f (K, T, N)

where total output (Q) is a function (f) of capital stock (K), technical knowledge (T), and the number of workers (N)

Given K and T, the production function becomes Q = f (AO which shows that output is a function of the number of workers. Output is an increasing function of the number of workers, output increases as the employment of labour rises. But after a point when more workers are employed, diminishing marginal returns to labour start.

This is shown in Fig. 1 where the curve Q = f (N) is the production function and the total output OQ1 corresponds to the full employment level NF. But when more workers NfN2 are employed beyond the full employment level of output OQ1, the increase in output Q1Q2 is less than the increase in employment N1N2.

Dia 1

Labour Market Equilibrium:

In the labour market, the demand for labour and the supply of labour determine the level of output and employment. The classical economists regard the demand for labour as the function of the real wage rate: DN =f (W/P)Where DN = demand for labour, W = wage rate and P = price level. Dividing wage rate (W) by price level (P), we get the real wage rate (W/P).

The demand for labour is a decreasing function of the real wage rate, as shown by the downward sloping DN curve in Fig. 2. It is by reducing the real wage rate that more workers can be employed.

Dia2

The supply of labour also depends on the real wage rate: SN =f (W/P), where SN is the supply of labour. But it is an increasing function of the real wage rate, as shown by the upward sloping SN curve in Fig. 2. It is by increasing the real wage rate that more workers can be employed.

When the DN and SN curves intersect at point E, the full employment level NF is determined at the equilibrium real wage rate W/P0. If the wage rate rises from WP0 to WP1 the supply of labour will be more than its demand by ds.

Now at W/P1 wage rate, ds workers will be involuntary unemployed because the demand for labour (W/P1-d) is less than their supply (W/P1-s). With competition among workers for work, they will be willing to accept a lower wage rate. Consequently, the wage rate will fall from W/P1 to W/P0.

The supply of labour will fall and the demand for labour will rise and the equilibrium point E will be restored along with the full employment level Nr On the contrary, if the wage rate falls from W/P0 to WP2 the demand for labour (W/P2-d1) will be more than its supply (W/P2-s1). Competition by employers for workers will raise the wage rate from W/ P2 to W/P0 and the equilibrium point E will be restored along with the full employment level NF.

Wage Price Flexibility:

The classical economists believed that there was always full employment in the economy. In case of unemployment, a general cut in money wages would take the economy to the full employment level. This argument is based on the assumption that there is a direct and proportional relation between money wages and real wages.

When money wages are reduced, they lead to reduction in cost of production and consequently to the lower prices of products. When prices fall, demand for products will increase and sales will be pushed up. Increased sales will necessitate the employment of more labour and ultimately full employment will be attained.

Pigou explains the entire proposition in the equation: N = qY/W. In this equation, N is the number of workers employed, q is the fraction of income earned as wages, Y is the national income and W is the money wage rate. N can be increased by a reduction in W. Thus the key to full employment is a reduction in money wage. When prices fall with the reduction of money wage, real wage is also reduced in the same proportion.

As explained above, the demand for labour is a decreasing function of the real wage rate. If W is the money wage rate, P is the price of the product, and MPN is the marginal product of labour, we have W=P X MPN or W/P = MPN

Since MPN declines as employment increases, it follows that the level of employment increases as the real wage (W/P) declines. This is explained in Figure 3. In Panel (A), SN is the supply curve of labour and DN is the demand curve for labour. The intersection of the two curves at E shows the level of full employment NF and the real wage W/P0.

If the real wage rises to W/P1, supply exceeds the demand for labour by sd and N1N2 workers are unemployed. It is only when the wage is reduced to W/P0 that unemployment disappears and the level of full employment is attained.

Dia3

This is shown in Panel (B), where MPN is the marginal product of labour curve which slopes downward as more labour is employed. Since every worker is paid wages equal to his marginal product, therefore the full employment level NF is reached when the wage rate falls from W/P1 to W/P0.

Contrariwise, with the fall in the wage from W/P0 to W/P2, the demand for labour increases more than its supply by s1d1, the workers demand higher wage. This leads to the rise in the wage from W/P2 to W/P0 and the full employment level NF is attained.

Goods Market Equilibrium:

The goods market is in equilibrium when saving equals investment. At that point of time, total demand equals total supply and the economy is in a state of full employment. According to the classicists, what is not spent is automatically invested.

Thus saving must equal investment. If there is any divergence between the two, the equality is maintained through the mechanism of the rate of interest. To them, both saving and investment are the functions of the interest rate.

S=f(r) …(1)

I=f(r) …(2)

S = I

Where S = saving, I = investment, and r = interest rate.

To the classicists, interest is a reward for saving. The higher the rate of interest, the higher the saving, and lower the investment. On the contrary, the lower the rate of interest, the higher the demand for investment funds, and lowers the saving. If at any given period, investment exceeds saving, (I > S) the rate of interest will rise.

Saving will increase and investment will decline till the two are equal at the full employment level. This is because saving is regarded as an increasing function of the interest rate and investment as a decreasing function of the rate of interest.

Assuming interest rates are perfectly elastic, the mechanism of the equality between saving and investment is shown in Figure 4 where S is the saving curve and I is the investment curve. Both intersect at E which is the full employment level where at Or interest rate S = I. If the interest rate rises to Or1 saving is more than investment by ha which will lead to unemployment in the economy.

Dig4

Since S > I, the investment demand for capital being less than its supply, the interest rate will fall to Or, investment will increase and saving will decline. Consequently, S = I equilibrium will be re-established at point E.

On the contrary, with a fall in the interest rate from Or to Or2 investment will be more than saving (I > S) by cd, the demand for capital will be more than its supply. The interest rate will rise, saving will increase and investment will decline. Ultimately, S = I equilibrium will be restored at the full employment level E.

Money Market Equilibrium:

The money market equilibrium in the classical theory is based on the Quantity Theory of Money which states that the general price level (P) in the economy depends on the supply of money (M). The equation is MV= PT, where M = supply of money, V= velocity of circulation of M, P = Price level, and T = volume of transaction or total output.

The equation tells that the total money supply MV equals the total value of output PT in the economy. Assuming V and T to be constant, a change in the supply of money (M) causes a proportional change in the price level (P). Thus the price level is a function of the money supply: P = f (M).

The relation between quantity of money, total output and price level is depicted in Figure 5 where the price level is taken on the horizontal axis and the total output on the vertical axis. MV is the/money supply curve which is a rectangular hyperbola.

This is because the equation MV = PT holds on all points of this curve. Given the output level OQ, there would be only one price level OP consistent with the quantity of money, as shown by point M on the MV curve. If the quantity of money increases, the MV curve will shift to the right as M1V curve.

Dia 5

As a result, the price level would rise from OP to OP1 given the same level of output OQ. This rise in the price level is exactly proportional to the rise in the quantity of money, i.e., PP1 = MM1 when the full employment level of output remains OQ.

2. Complete Classical Model – A Summary:

The classical theory of employment was based on the assumption of full employment where full employment was a normal situation and any deviation from this was regarded as an abnormal situation. This was based on Say’s Law of Market.

According to this, supply creates its own demand and the problem of overproduction and unemployment does not arise. Thus there is always full employment in the economy. If there is overproduction and unemployment, the automatic forces of demand and supply in the market will bring back the full employment level.

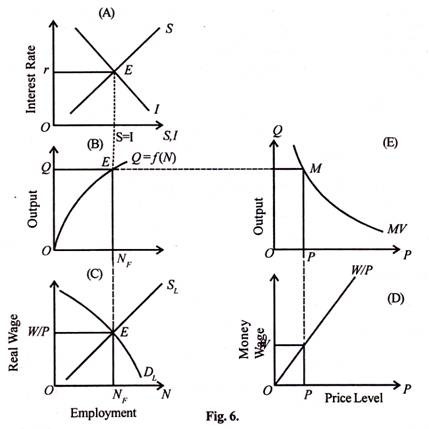

In the classical theory, the determination of output and employment takes place in labour, goods and money markets of the economy, as shown in Fig. 6. The forces of demand and supply in these markets will ultimately bring full employment in the economy.

Dia6

In the classical analysis, output and employment in the economy are determined by the aggregate production function, demand for labour and supply of labour. Given the stock of capital, technical knowledge and other factors, there is a precise relation between total output and employment (number of workers).

This is expressed as Q = f (K, T, N). In other words, total output (Q) is a function (f) of capital stock (K), technical knowledge T, and number of workers (TV). Given K and T, total output (Q) is an increasing function of the number of workers (N): Q=f (N) as shown in Panel (B). At point E, ONF workers produce OQ output. But beyond point E, as more workers are employed, diminishing marginal returns start.

Labour Market Equilibrium:

In the labour market, the demand for and supply of labour determine output and employment in the economy. The demand for labour depends on total output. As production increases, the demand for labour also increases.

The demand for labour, in turn, depends on the marginal productivity (MP) of labour which declines as more workers are employed. The supply of labour depends on the wage rate, SL = f (W/P), and is an increasing function of the wage rate.

The demand for labour also depends on the wage rate, DL =f (W/P), and is a decreasing function of the wage rate. Thus both the demand for and supply of labour are the functions of real wage rate (W/P). The intersection point E of DL and SL curves at W/ P wage rate in Panel (C) of the figure determines the full employment level ONF.

Goods Market Equilibrium:

In the classical analysis, the goods market is in equilibrium when saving and investment are in equilibrium (S=I). This equality is brought about by the mechanism of interest rate at the full employment level of output so that the quantity of goods demanded is equal to the quantity of goods supplied. This is shown in Panel (A) of the figure where S=I at point E when the interest rate is Or.

Money Market Equilibrium:

The money market is in equilibrium when the demand for money equals the supply of money. This is explained by the Quantity Theory of Money which states that the quantity of money is a function of the price level, P=f (MV). Changes in the general price level are proportional to the quantity of money.

The equilibrium in the money market is shown by the equation MV = PT where MV is the supply of money and PT is the demand for money. The equilibrium of the money market explains the price level corresponding to the full employment level of output which relates Panel (E) and Panel (B) with MQ line.

The price level OP is determined by total output (Q) and the quantity of money (MV), as shown in Panel (E). Then the real wage corresponding with the money wage is determined by the (W/P) curve, as shown in Panel (D).

When the money wage increases, the real wage also increases in the same proportion and there is no effect on the level of output and employment. It follows that the money wage should be reduced in order to attain the full employment level in the economy. Thus the classicists favoured a flexible price-wage policy to maintain full employment.

Keynes vehemently criticised the classical theory of employment for its unrealistic assumptions in his General Theory.

He attacked the classical theory on the following counts:

(1) Underemployment Equilibrium:

Keynes rejected the fundamental classical assumption of full employment equilibrium in the economy. He considered it as unrealistic. He regarded full employment as a special situation. The general situation in a capitalist economy is one of underemployment.

This is because the capitalist society does not function according to Say’s law, and supply always exceeds its demand. We find millions of workers are prepared to work at the current wage rate, and even below it, but they do not find work.

Thus the existence of involuntary unemployment in capitalist economies (entirely ruled out by the classicists) proves that underemployment equilibrium is a normal situation and full employment equilibrium is abnormal and accidental.

(2) Refutation of Say’s Law:

Keynes refuted Say’s Law of markets that supply always created its own demand. He maintained that all income earned by the factor owners would not be spent in buying products which they helped to produce.

A part of the earned income is saved and is not automatically invested because saving and investment are distinct functions. So when all earned income is not spent on consumption goods and a portion of it is saved, there results in a deficiency of aggregate demand.

This leads to general overproduction because all that is produced is not sold. This, in turn, leads to general unemployment. Thus Keynes rejected Say’s Law that supply created its own demand. Instead he argued that it was demand that created supply. When aggregate demand rises, to meet that demand, firms produce more and employ more people.

(3) Self-adjustment not Possible:

Keynes did not agree with the classical view that the laissez-faire policy was essential for an automatic and self-adjusting process of full employment equilibrium. He pointed out that the capitalist system was not automatic and self-adjusting because of the non-egalitarian structure of its society. There are two principal classes, the rich and the poor.

The rich possess much wealth but they do not spend the whole of it on consumption. The poor lack money to purchase consumption goods. Thus there is general deficiency of aggregate demand in relation to aggregate supply which leads to overproduction and unemployment in the economy. This, in fact, led to the Great Depression.

Had the capitalist system been automatic and self-adjusting, this would not have occurred. Keynes, therefore, advocated state intervention for adjusting supply and demand within the economy through fiscal and monetary measures.

(4) Equality of Saving and Investment through Income Changes:

The classicists believed that saving and investment were equal at the full employment level and in case of any divergence the equality was brought about by the mechanism of rate of interest. Keynes held that the level of saving depended upon the level of income and not on the rate of interest.

Similarly investment is determined not only by rate of interest but by the marginal efficiency of capital. A low rate of interest cannot increase investment if business expectations are low. If saving exceeds investment, it means people are spending less on consumption.

As a result, demand declines. There is overproduction and fall in investment, income, employment and output. It will lead to reduction in saving and ultimately the equality between saving and investment will be attained at a lower level of income. Thus it is variations in income rather than in interest rate that bring the equality between saving and investment.

(5) Importance of Speculative Demand for Money:

The classical economists believed that money was demanded for transactions and precautionary purposes. They did not recognise the speculative demand for money because money held for speculative purposes related to idle balances.

But Keynes did not agree with this view. He emphasised the importance of speculative demand for money. He pointed out that the earning of interest from assets meant for transactions and precautionary purposes may be very small at a low rate of interest.

But the speculative demand for money would be infinitely large at a low rate of interest. Thus the rate of interest will not fall below a certain minimum level, and the speculative demand for money would become perfectly interest elastic. This is Keynes ‘liquidity trap’ which the classicists failed to analyse.

(6) Rejection of Quantity Theory of Money:

Keynes rejected the classical Quantity Theory of Money on the ground that increase in money supply will not necessarily lead to rise in prices. It is not essential that people may spend all extra money. They may deposit it in the bank or save.

So the velocity of circulation of money (V) may slow down and not remain constant. Thus V in the equation MV = PT may vary. Moreover, an increase in money supply, may lead to increase in investment, employment and output if there are idle resources in the economy and the price level (P) may not be affected.

(7) Money not Neutral:

The classical economists regarded money as neutral. Therefore, they excluded the theory of output, employment and interest rate from monetary theory. According to them, the level of output and employment and the equilibrium rate of interest were determined by real forces.

Keynes criticised the classical view that monetary theory was separate from value theory. He integrated monetary theory with value theory, and brought the theory of interest in the domain of monetary theory by regarding the interest rate as a monetary phenomenon. He integrated the value theory and the monetary theory through the theory of output.

This he did by forging a link between the quantity of money and the price level via the rate of interest. For instance, when the quantity of money increases, the rate of interest falls, investment increases, income and output increase, demand increases, factor costs and wages increase, relative prices increase, and ultimately the general price level rises. Thus Keynes integrated monetary and real sectors of the economy.

(8) Refutation of Wage-Cut:

Keynes refuted the Pigovian formulation that a cut in money wage could achieve full employment in the economy. The greatest fallacy in Pigou’s analysis was that he extended the argument to the economy which was applicable to a particular industry.

Reduction in wage rate can increase employment in an industry by reducing costs and increasing demand. But the adoption of such a policy for the economy leads to a reduction in employment. When there is a general wage-cut, the income of the workers is reduced. As a result, aggregate demand falls leading to a decline in employment.

From the practical view point also Keynes never favoured a wage cut policy. In modern times, workers have formed strong trade unions which resist a cut in money wage. They would resort to strikes. The consequent unrest in the economy would bring a decline in output and income. Moreover, social justice demands that wages should not be cut if profits are left untouched.

(9) No Direct and Proportionate Relation between Money and Real Wages:

Keynes also did not accept the classical view that there was a direct and proportionate relationship between money wages and real wages. According to him, there is an inverse relation between the two. When money wages fall, real wages rise and vice versa.

Therefore, a reduction in the money wage would not reduce the real wage, as the classicists believed, rather it would increase it. This is because the money wage cut will reduce cost of production and prices by more than the former.

Thus the classical view that fall in real wages will increase employment breaks down. Keynes, however, believed that employment could be increased more easily through monetary and fiscal measures rather than by reduction in money wage. Moreover, institutional resistances to wage and price reductions are so strong that it is not possible to implement such a policy administratively.

(10) State Intervention Essential:

Keynes did not agree with Pigou that “frictional maladjustments alone account for failure to utilise fully our productive power.” The capitalist system is such that left to itself it is incapable of using productive powerfully. Therefore, state intervention is necessary.

The state may directly invest to raise the level of economic activity or to supplement private investment. It may pass legislation recognising trade unions, fixing minimum wages and providing relief to workers through social security measures.

“Therefore”, as observed by Dillard, “it is bad politics even if it should be considered good economics to object to labour unions and to liberal labour legislation.” So Keynes favoured state action to utilise fully the resources of the economy for attaining full employment.

(11) Long-Run Analysis Unrealistic:

The classicists believed in the long-run full employment equilibrium through a self-adjusting process. Keynes had no patience to wait for the long period for he believed that “In the long-run we are all dead”.

As pointed by Schumpeter, “His philosophy of life was essentially a short-term philosophy.” His analysis is confined to short-run phenomena. Unlike the classicists, he assumes tastes, habits, techniques of production, supply of labour, etc. to be constant during the short period and so neglects long-run influences on demand.

Assuming consumption demand to be constant, he lays emphasis on increasing investment to remove unemployment. But the equilibrium level so reached is one of underemployment rather than of full employment. Thus the classical theory of employment is unrealistic and is incapable of solving the present day economic problems of the capitalist world.